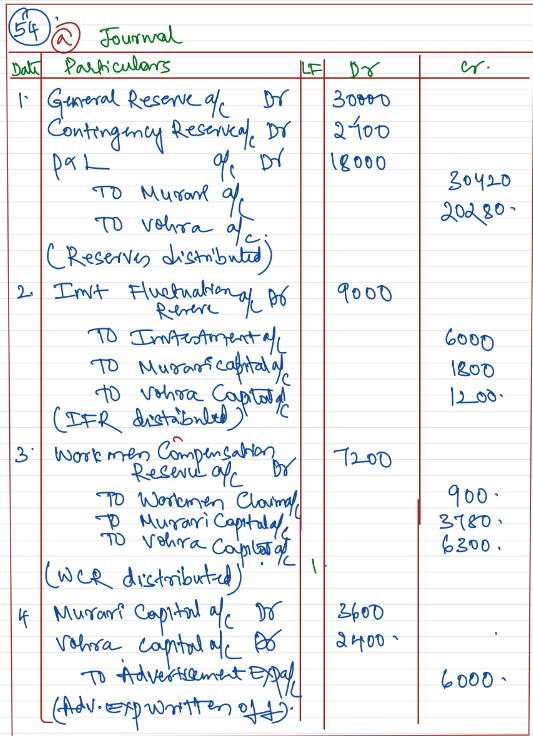

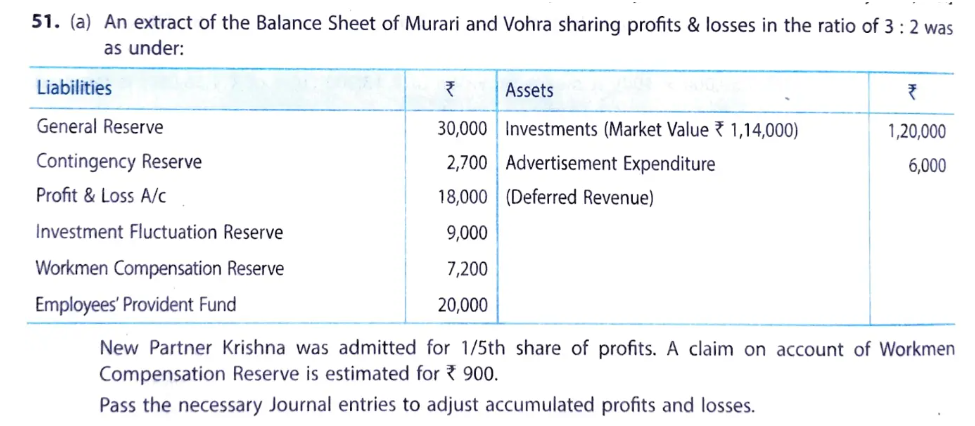

a) An extract of the Balance Sheet of Murari and Vohra sharing profits and losses in the ratio of 3 : 2 was as under:

| Liabilities | ₹ | Assets | ₹ |

| General Reserve Contingency Reserve Profit & Loss A/c Investment Fluctuation Reserve Workmen Compensation Reserve Employees Provident Fund |

30,000 2,700 18,000 9,000 7,200 20,000 |

Investments (Market Value ₹ 1,14,000) Advertisement Expenditure (Deferred Revenue) |

1,20,000 6,000 |

New Partner Krishna was admitted for 1/5th share of profits. A claim on account of workmen Compensation Reserve is estimated for ₹ 900.

Pass the necessary Journal entries to adjust accumulated profits and losses.

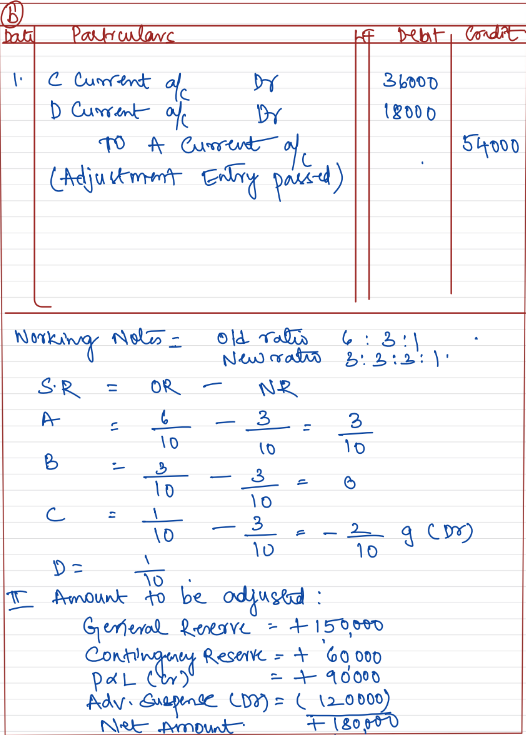

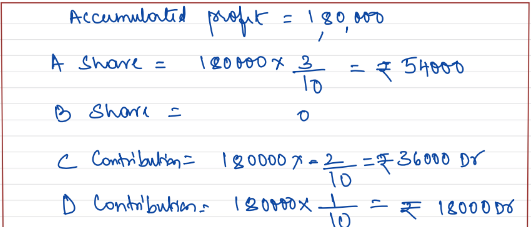

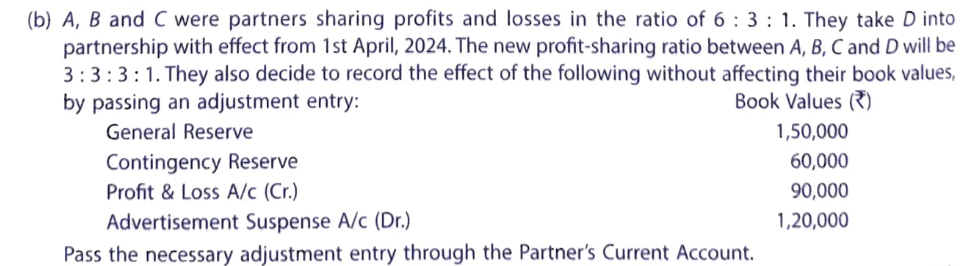

(b) A, B and C were partners sharing profits and losses in the ratio of 6 : 3 : 1. They take D into partnership with effect from 1st April, 2023. The new profit sharing ratio between A, B, C and D will be 3 : 3 : 3 : 1. They also decide to record the effect of the following without affecting their book values by passing an adjusting entry:

Solution :

| Book Value (₹) | |

| General Reserve | 1,50,000 |

| Contingency Reserve | 60,000 |

| Profit & Loss A/c (Cr.) | 90,000 |

| Advertisement Suspense A/c (Dr.) | 1,20,000 |

Pass the necessary adjustment entry through the Partner’s Current Account.