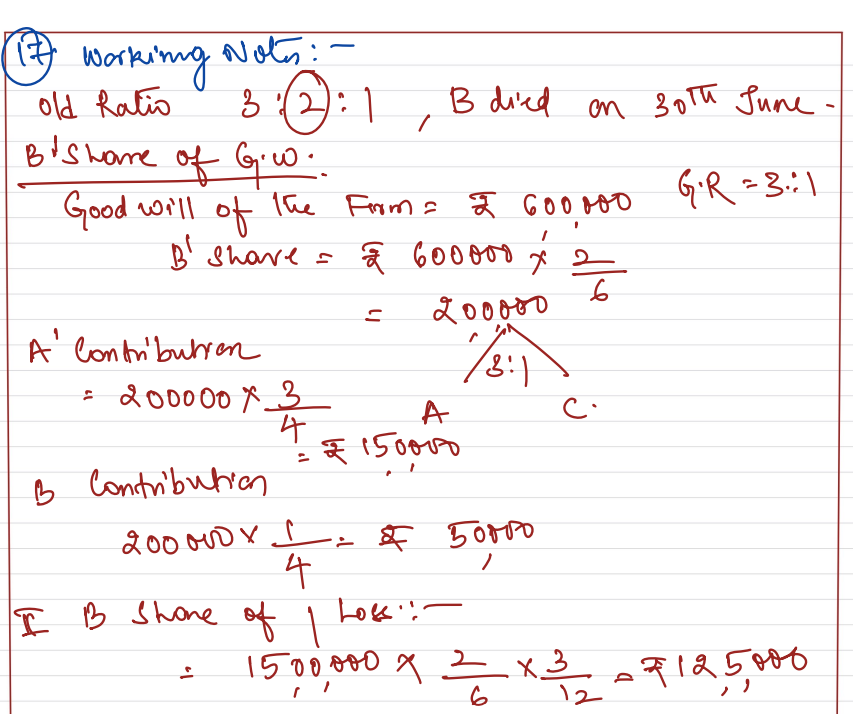

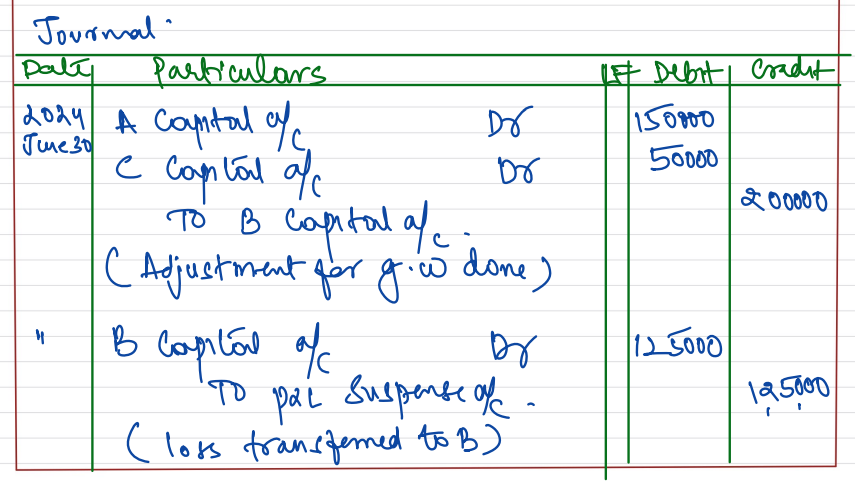

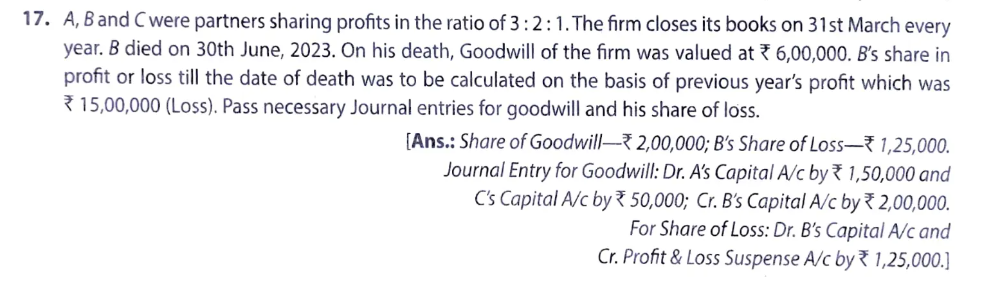

A, B and C were partners sharing profits in the ratio of 3 : 2 : 1. The firm closes its books on 31st March every year. B died on 30th June, 2022. On his death, Goodwill of the firm valued at ₹ 6,00,000. B’s share in profit or loss till the date was to be calculated on the basis of previous year’s profit which was ₹ 15,00,000 (Loss). Pass necessary Journal entries for goodwill and his share of loss.

[Ans. Share of Goodwill – ₹ 2,00,000; B’s Share of Loss – ₹ 1,25,000. Journal Entry for Goodwill: Dr. A’s Capital A/c by ₹ 1,50,000 and C’s Capital A/c by ₹ 50,000; Cr. B’s Capital A/c by ₹ 2,00,000. For Share of Loss: Dr. B’s Capital A/c and Cr. Profit & Loss Suspense A/c by ₹ 1,25,000.

Solution:-