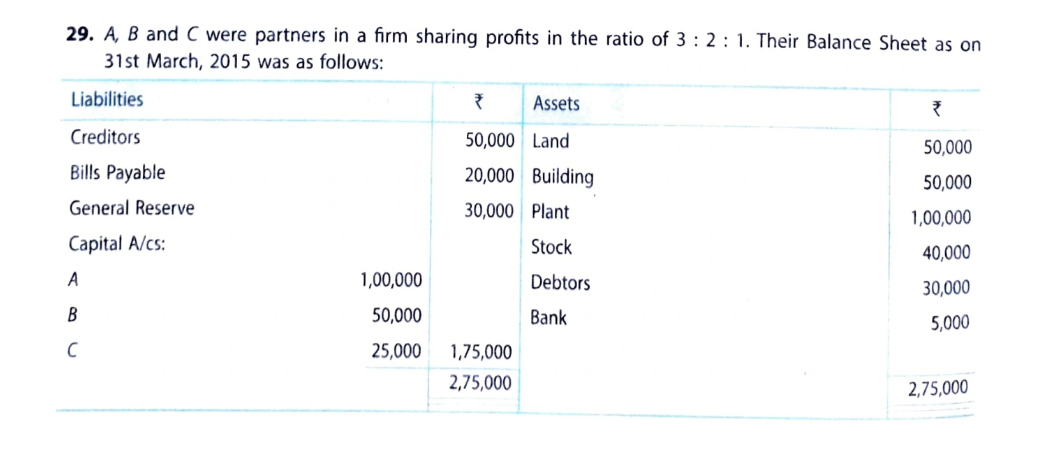

A, B and C were partners in a firm sharing profits in the ratio of 3 : 2 : 1. Their Balance Sheet as on 31st March, 2015 was as follows:

| Liabilities | ₹ | Assets | ₹ |

| Creditors Bills Payable General Reserve Capital A/cs: A B C |

50,000 20,000 30,0001,00,000 50,000 25,000 |

Land Building Plant Stock Debtors Bank |

50,000 50,000 1,00,000 40,000 30,000 5,000 |

| 2,75,000 | 2,75,000 |

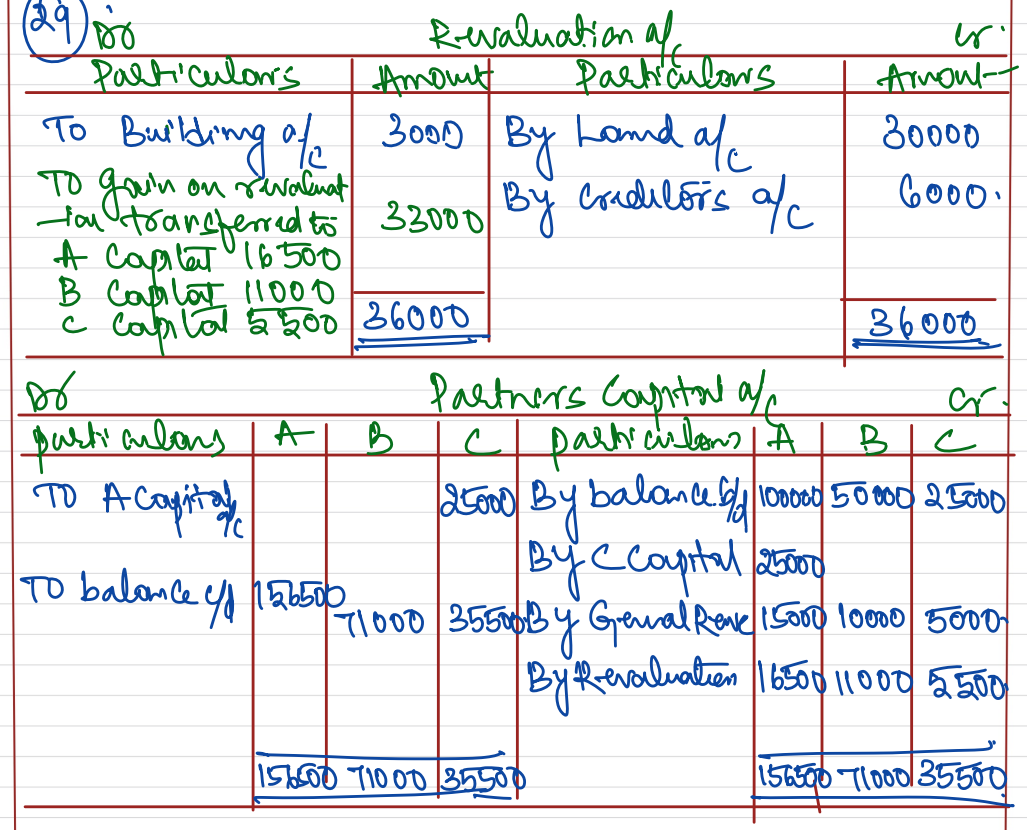

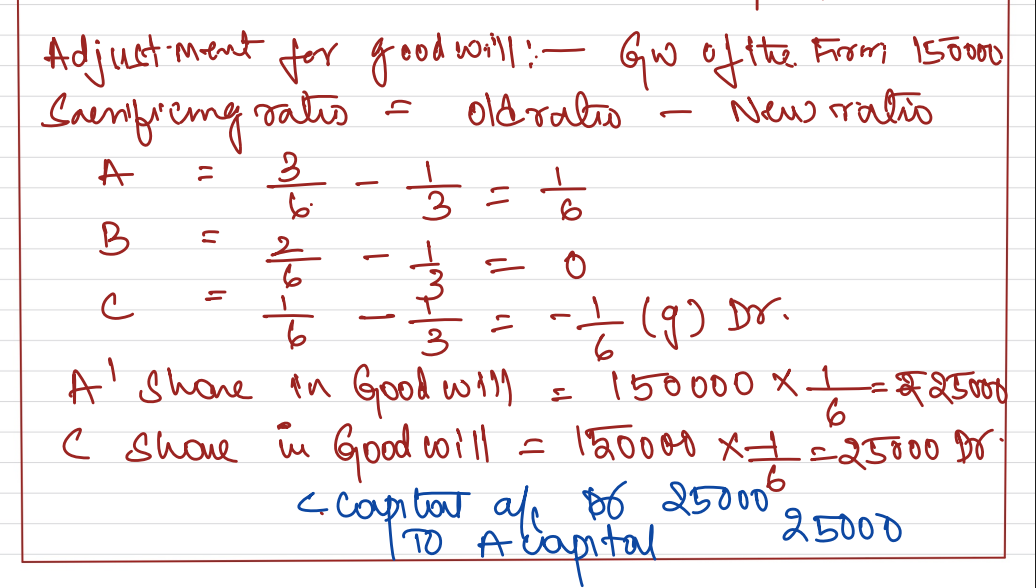

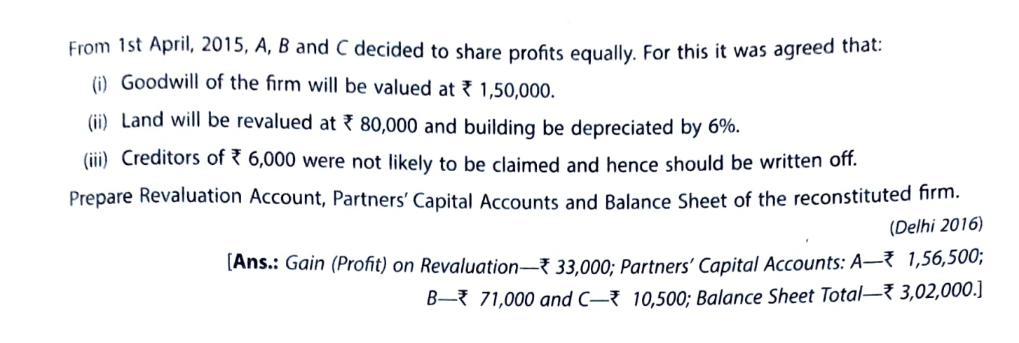

From 1st April, 2015, A, B and C decided to share profits equally. For this it was agreed that:

i) Goodwill of the firm will be valued at ₹ 1,50,000.

ii) Land will be revalued at ₹ 80,000 and building be decpreciated by 6%

iii) Creditors of ₹ 6,000 were not likely to be claimed and hence should be written off.

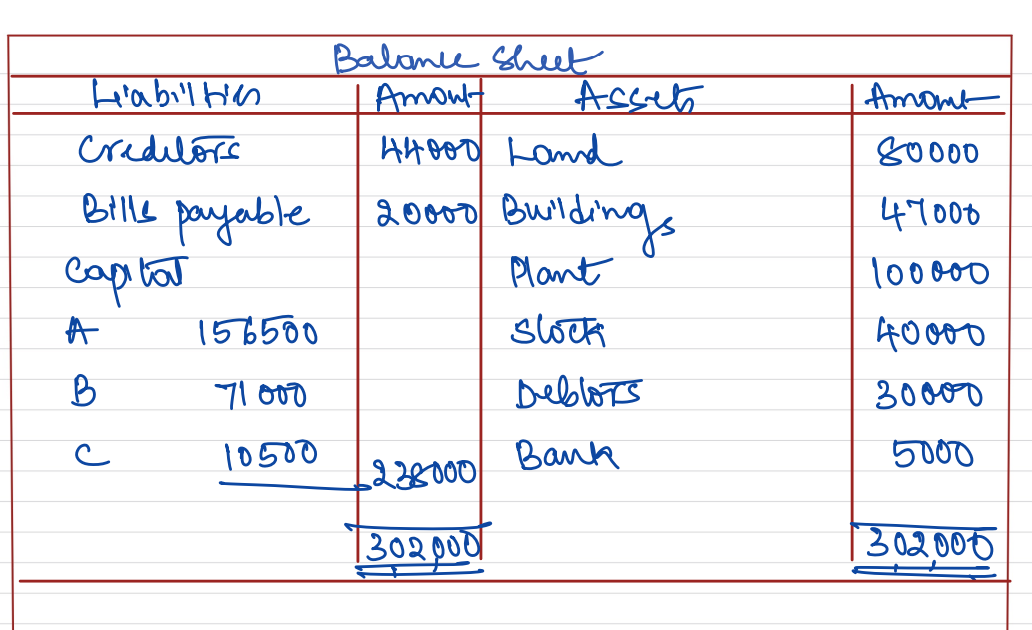

Prepare Revaluation Account, Partner’s Capital Accounts and Balance Sheet of the reconstituted firm.

[Ans.: Gain (Profit) on Revaluation – ₹ 33,000; Partner’s Capital Accoufnts: A – ₹ 1,56,000; B – ₹ 71,000 and C – ₹ 10,500; Balance Sheet Total – ₹ 3,02,000.]

Solution:-