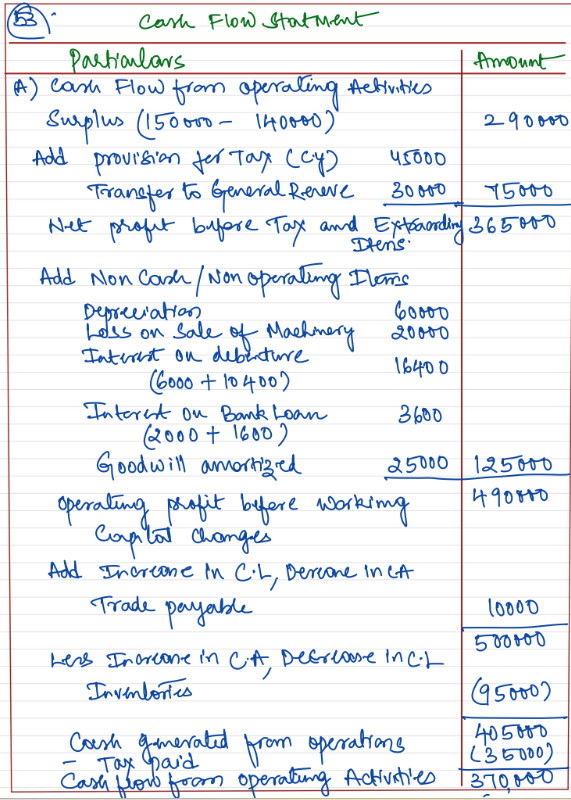

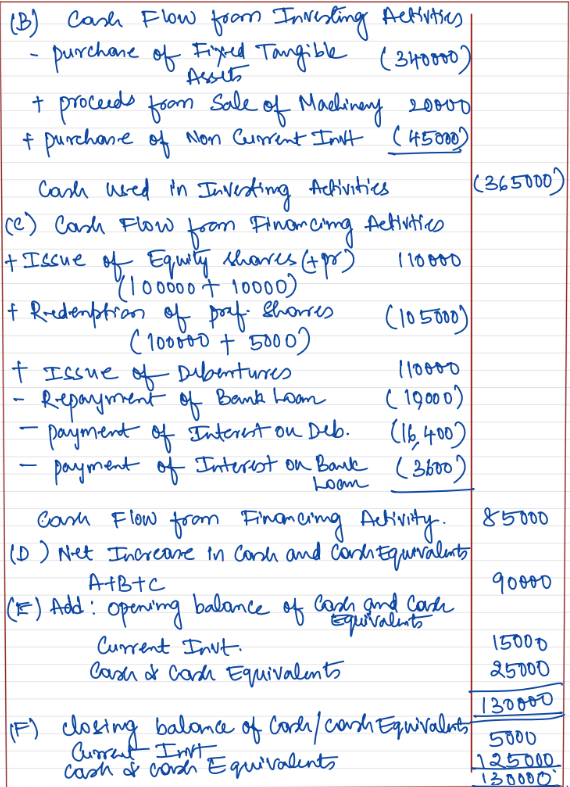

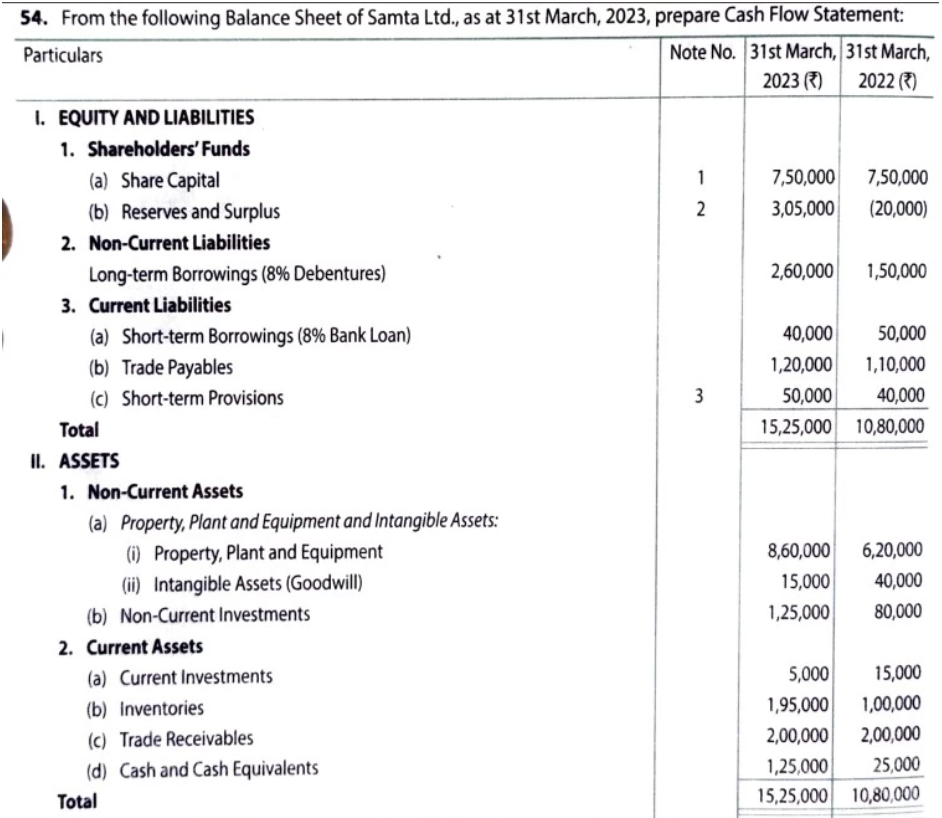

From the following Balance Sheet of Samta Ltd., as at 31st March, 2023, prepare Cash Flow Statement:

| Particulars | 31st March, 2023 (₹) |

31st March, 2022 (₹) |

| I. EQUITY AND LIABILITIES | ||

| 1. Shareholder’s Funds (a) Share Capital (b) Reserves and Surplus |

7,50,000 3,05,000 |

7,50,000 (20,000) |

| Non-Current Liabilities Long-term Borrowings (8% Debentures) |

2,60,000 | 1,50,000 |

| Current Liabilities (a) Short-term Borrowings (8% Bank Loan) (b) Trade Payables (c) Short-term Provisions |

40,000 1,20,000 50,000 |

50,000 1,10,000 40,000 |

| Total | 15,25,000 | 10,80,000 |

| II. Assets | ||

| Non-Current Assets (a) Property, Plant and Equipment and Intangible Assets: (i) Property, Plant and Equipment (ii) Intangible Assets (Goodwill) (b) Non-Current Investments |

8,60,000 15,000 1,25,000 |

6,20,000 40,000 80,000 |

| Current Assets (a) Current Investments (b) Inventories (c) Trade Receivables (d) Cash and Cash Equivalents |

5,000 1,95,000 2,00,000 1,25,000 |

15,000 1,00,000 2,00,000 25,000 |

| Total | 15,25,000 | 10,80,000 |

| Particulars | 31st March, 2023 (₹) |

31st March, 2022 (₹) |

|

| Share Capital Equity Sahre Capital 10% Preference Share Capital |

5,50,000 2,00,000 |

4,50,000 3,00,000 |

|

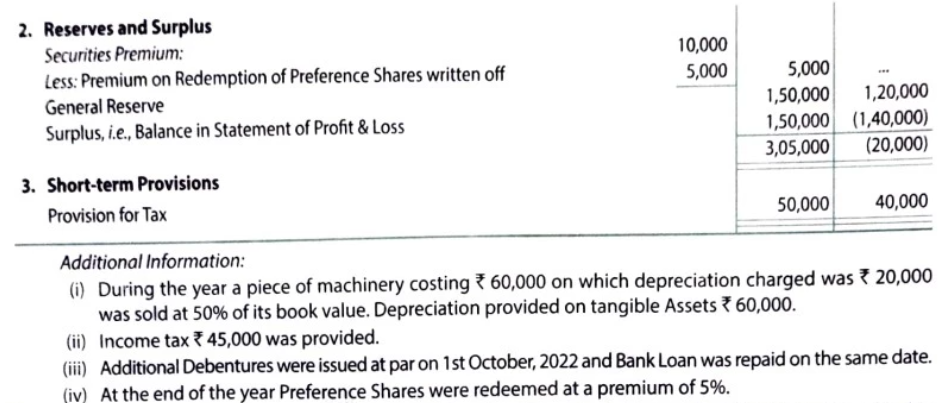

| Reserves and Surplus Securities Premium: Less: Premium on Redemption of Preference Shares written off General Reserve Surplus, i.e., Balance in Statement of Profit & Loss |

10,000 5,000 |

5,000 1,50,000 1,50,000 |

– 1,20,000 (1,40,000) |

| Short-term Provisions Provision for Tax |

50,000 | 40,000 |

Additional Information:

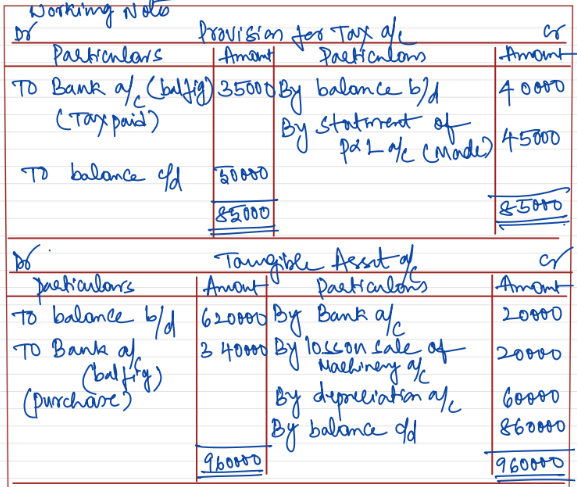

- During the year a piece of machinery costing ₹ 60,000 on which depreciation charged was ₹ 20,000 was sold at 50% of its book value. Depreciation provided on tangible Assets ₹ 60,000.

- Income Tax ₹ 45,000 was provided.

- Additonal Debentures were issued at par on 1st October, 2022 and Bank Loan was repaid on the same date.

- At the end of the year Preference Shares were redeemed at a premium of 5%.

Solution :